Jack Bogle pioneered the investing world and the mutual fund industry. He taught the world that they should not be paying fees for performance, and that seeking to be average will outperform over the medium-term and the long-term. He was correct that the extraordinary performance of a single manager is seldom, if ever, sustainable and that their fees will exact major damage for the investor.

I have been amazed that the best business schools in the country – Columbia, Harvard and Stanford – are still full of aspiring analysts and money managers in the post-Vanguard era. all still seeking to open their own funds. More amazing is that many of these folks are still successful in raising capital (many aren’t).

Ever since I co-founded BestCashCow, I have frequently been asked if it is my view that people should avoid the stock market. That has never been my view. Over the long-term, investing in a broad and diversified stock market portfolio, and only just matching the stock market is the single best way to build wealth. My view is that you should never be 100% in the stock market and that you will never know when you will require liquidity. I’ve now lived long enough to know that many who were overinvested and forced to sell in October 1987, early 2001 or early 2009 were, without exaggeration, slaughtered.

So, while you should never be 100% in the market, you should be in the market in some form. And, for those who don’t know how to build their own portfolio through an online broker, an extremely low fee fund like the Vanguard S&P 500 Index is a much better way than to pay fees upon fees upon fees to invest with someone who has put together a couple of good years at the track. And, running parallel with forays into the market, of course, must be the wisdom to keep resources out of the market and in savings and CDs. It’s that dual strategy that will always be a winning strategy.

Occasionally, financial planners reach out to me and want to connect on LinkedIn and social media. While I do not hold financial planners in very high esteem since, they are always selling their latest product. I occasionally connect in order to further the reach of BestCashCow.

I do not often engage in debate with these folks, but sometimes I see information shared that is so dangerous to investors and their retirement planning that I need to say something.

As dangerous as individual bonds may be, they are in principle much less dangerous than owning a bond fund, even a high quality bond fund, since you can always just hold a bond until maturity without having your proceeds drained by a manager in a down environment. At maturity, you get out at par, whereas you may never get out of a bond fund at par.

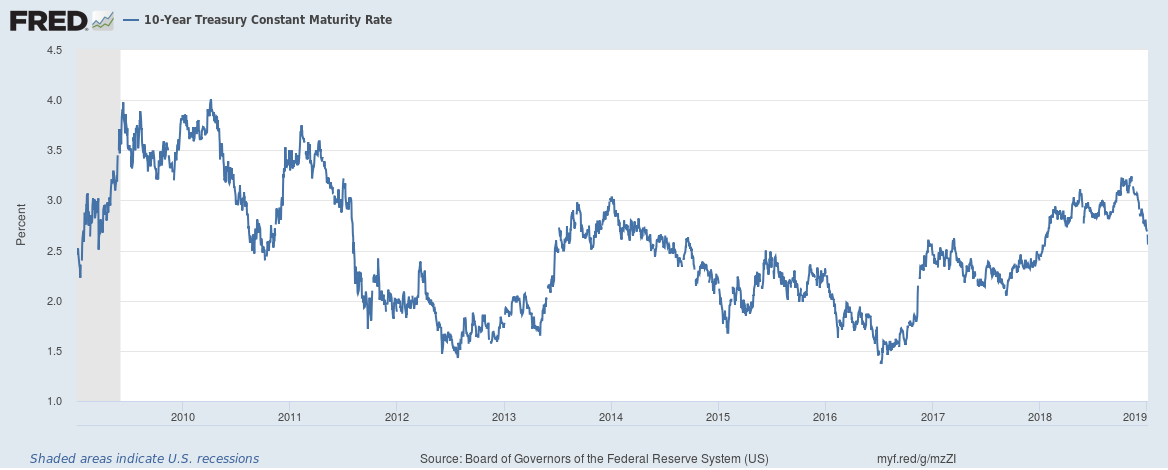

The 10-year US Treasury went to 3.20% last year. As interest rates rose, bond prices fell. Market turmoil over the last 2 months has lead people to seek safe haven in bonds and that has brought US Treasury rates back to 2.60%. But, this is a blip. It is a fleeting moment where you should be selling bonds and bond funds. It isn’t a time to buy. The Federal Reserve is still normalizing interest rates and in that environment the 10-year is still going up.

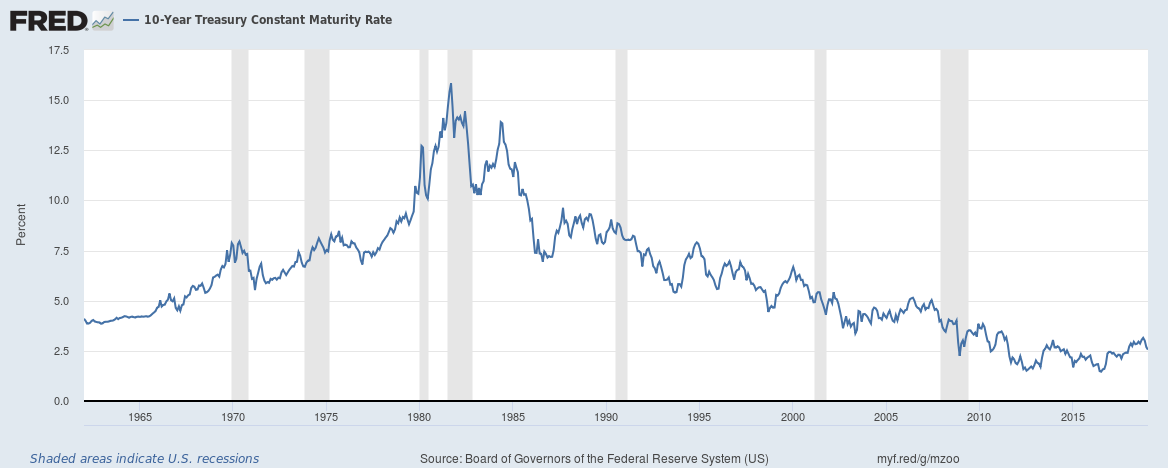

These two graphs from the St. Louis Fed are the best warning I can give. The first, that dates back to 1960, shows how abnormally compressed the 10-year Treasury is by any long-term measure. The second, dating back only 10 years, shows how quickly 10-year US Treasury rates can reverse and rise (even in an environment where interest rates are low).

The “buy bond funds” crowd came out of the woodwork in dramatic fashion in mid-2010 as the 10-year fell from 4.00% to 2.50%. Those who followed this advice saw their funds collapse when interest rates reversed and were in a world of pain in January 2011. While those folks found some opportunities to get out later, opportunities which buyers today may not get.

I cannot do it anymore. I just cannot watch CNBC or Bloomberg. It isn’t because the market is falling (it is). And, it isn’t because I cannot bear to hear the usual batch of cheerleaders (so-called “analysts”) extolling the virtues of being long in an uncertain time.

Unlike 99% of the analysts, Joe Lavorgna is about as reasoned of an analyst as CNBC ever has as a guest. Yet, he too denies inflation and says that the Fed needs to relent and “let the economy run hot.”

The problem with Lavorgna’s reasoning is clear: the Fed has a dual mandate of full employment and price stability. Price stability is achieved by fighting inflation and ensuring that the real value of the US currency maintains its current level of purchasing power. If $100 today becomes $102 in a year, but has the purchasing power of $90 today, the economy falters. People need to earn enough in their savings accounts and other risk-free investments in order to ensure that they don’t lose the value of their money because that will cause the wealth of the nation (and consumer confidence) to collapse.

Were Chairman Jay Powell to allow the Federal Reserve’s mandate to become the growth in the stock market (as Wall Street would like) and cheap borrowing costs for real estate developers (as the President would like), the Federal Reserve would be risking a diminution in our nation’s wealth in order to get a continued rally in the stock market.

But, Wall Street’s cheerleaders are pushing for this short-term gain over long-term economic security when they try to explain that there is no inflation.

Let’s clear this up:

First, there is inflation. Annual rates of inflation are calculated based on the Consumer Price Index, issued monthly by the Labor Department’s Bureau of Labor Statistics. The CPI number issued on December 12, 2018 indicates a move from 246.669 to 252.038 from November 2017 to November 2018 for an inflation rate of 2.20%. This rate is still historically low, although much higher than the measure for the last several years.

The CPI indicator is controversial for many reasons, but one thing that economists universally agree upon is that it is backward looking. The Fed, therefore, looks at a variety of other factors many of which are going to try to measure incipient inflation.

Second, there are all sorts of reasons to believe we could have serious inflation in 2019 that will not show up until it is here.

I see at least four significant inflationary pressures in 2019 that weren’t present in 2018.

Continuation or escalation of the trade war with China is inflationary as we have long relied on China for all sorts of low cost items and inputs. Tariffs placed on those items will cause the cost of goods to increase or purchasers to find alternative - and more expensive – replacements.

Brexit and its March 29, 2019 deadline present a range of possible outcomes. A hard Brexit or anything that might resemble it will be tragic for the British economy, but the disruption that it will cause in global markets will be inflationary.

Commodity prices collapsed in the second half of 2018. If oil does anything other than continues to fall in a straight line, transportation costs will increase. If other commodities bounce, input costs will rise.

Minimum wage has just increased on January 1, 2019 in 20 states (including California and Florida) and a bunch of other cities (including DC). This affects the wages of 17 million people. In New York City, the cost of employing someone is now $15 an hour. If you don’t think that higher wages get passed on in the form of higher costs, come visit New York.

When analysts stop their market cheerleading and look at the same risks that the Federal Reserve and Jerome Powell are looking at, the inevitable conclusion is that the Fed needs to continue to hike rates in 2019.